Notifications 7

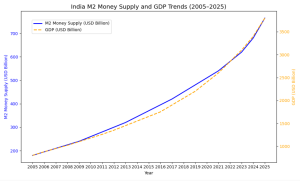

In May 2025, the U.S. M2 money supply reached an unprecedented $21.9 trillion, while India’s M2 stood at ₹67.73 trillion (~$765bn). These figures reflect decades of monetary expansion driven by economic crises, policy interventions, and evolving financial systems. But what does this surge in liquidity mean for markets, interest rates, inflation, and long-term economic planning?

Money supply refers to the total amount of money circulating in an economy at a given point in time. It includes physical currency, demand deposits, and other liquid assets. Economists and central banks track money supply to understand liquidity conditions and guide monetary policy.

Liquidity refers to the ease with which assets can be converted into cash without affecting their price. A high money supply, especially M2, which includes cash, savings deposits, and money market instruments means more money is available in the economy.

Why Does Money Supply Matter?

Example: After the 2008 financial crisis and the COVID-19 pandemic, central banks globally used quantitative easing (QE) to inject liquidity. This helped stabilize economies but also inflated asset prices.

Increased liquidity tends to boost demand for financial assets:

When money supply increases faster than output, inflation can rise. To counter this, central banks may raise interest rates, which can cool demand but also slow growth. Central banks must balance liquidity with inflation control:

Example: In 2024-25, the rupee hovered around ₹83–85 per USD, influenced by oil prices, FPI flows, and global interest rate trends.

Inflation occurs when too much money chases too few goods. Productivity improvements and efficient supply chains can help offset this. While inflation has moderated post-pandemic, excess liquidity is still a latent risk:

Liquidity supports credit growth, which can fuel GDP if directed productively:

Conclusion: Navigating a Liquidity-Driven World

The surge in global and Indian money supply reflects both past economic interventions and future growth ambitions. While liquidity can support recovery and investment, it also brings risks-asset bubbles, inflation, and currency volatility.

For learners and market participants, understanding the basics of monetary economics is essential. Whether you’re analysing stock trends, evaluating bond yields, or planning long-term investments, keeping an eye on liquidity trends can provide valuable insights.

Author: Mr. Biharilal Deora, CFA, CIPM, FCA

When people hear the term “risk management,” they often associate it with financial markets, insurance, or corporate governance. In…

As India charts its course towards Viksit Bharat, by 2047, the sophistication and depth of its financial markets are paramount.…

As investors, we often judge performance on monthly (MoM), Quarterly (QoQ) and year-on-year (YoY) statistics. It feels natural to look…

© 2025 National Institute of Securities Markets (NISM). All rights reserved.